What is an FHA Loan?

FHA home loans are federal assistance mortgages made by lenders, and backed by the government. The FHA doesn’t make loans to homeowners — it insures loans made to Iowa homeowners by federally-qualified lenders.

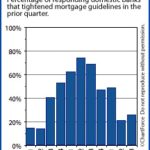

By all accounts, FHA home loans are surging in popularity.

- 2006, FHA insured 3.3% of all mortgages made

- Q2 2009, FHA insured 19.2% of all mortgages made

A major reason for the increase can be tied to guidelines.

As compared to its conforming mortgage cousins Fannie Mae and Freddie Mac, FHA home loans have lower downpayment requirements and looser credit standards. The FHA allows downpayments of 3.5 percent for homes in Urbandale and Fannie Mae and Freddie Mac do not, as an example.

Another reason is that FHA home loans aren’t subject to credit score fees the way that conforming mortgages are. Through Fannie or Freddie, a home buyer with a 650 FICO and 20% down is subject to 3% in risk fees. Via the FHA, the fee is zero, making FHA the better “deal”.

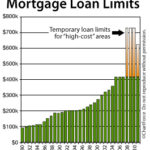

FHA Published 2010 Loan Limits

The base 2010 FHA loan limits are:

- 1-unit : $271,050

- 2-unit : $347,000

- 3-unit : $419,400

- 4-unit : $521,250

We say “base” because these loan limits don’t apply to all areas equally. Higher-cost regions get higher loan limits, based on typical home values. Homes in Los Angeles County, for example, can be FHA-insured up to $729,750 in 2010, and there are special exceptions made for Alaska and Hawaii.

The official FHA announcement included a complete, county-by-county FHA loan limit list. The first spreadsheet shows each county at or above the $729,750 maximum; the second list is everyone else.

If your home’s county is on neither list, use the “base” numbers above.

{ 1 comment… read it below or add one }

It’s in fact very complicated in this busy life to listen news on Television, so I just use the web for that purpose, and take the latest news.

Lorene