SURPRISE!!! Be Aware of How Credit Scores Work!

Black Friday is just a couple of days away. It’s the official start of the 2010 Holiday Shopping Season. I used to be in the retail world as a young lad and the idea of people rushing through the doors makes me glad I’m in the (much more fun) mortgage business!

Black Friday is just a couple of days away. It’s the official start of the 2010 Holiday Shopping Season. I used to be in the retail world as a young lad and the idea of people rushing through the doors makes me glad I’m in the (much more fun) mortgage business!

This year in the retail world, sales are expected to top $111 billion and, already, businesses are vying for shoppers and their dollars. Newspaper circulars are getting larger, and in-store discounting is more common.

But one discount that shoppers should think twice about is the popular “Open A Charge Card, Save 20%” promotion. The short-term savings may be tempting, but the long-term costs may be huge. Seriously, they could be.

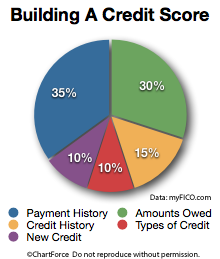

According to myFICO.com, “new credit” accounts for 85 out of 850 possible credit scoring points, with new credit defined by such traits as:

- Number of recently opened accounts

- Number of recent credit inquiries

- Time since recent credit inquiries

- Proportion of new accounts to all accounts

These traits are negatives against a FICO score so with each new, in-store credit card application, a person’s credit score will fall. The fall will be especially pronounced for persons lacking credit “depth”, or who have made a disproportionately large number of new credit applications recently.

Your Credit Score is Vital

For soon-to-be homeowners, or would-be refinancers in Ankeny, credit scores are worth keeping high. This is because credit scores change the mortgage rates and/or loan fees for which an applicant is eligible.

As an illustration, assuming 20% equity on a $200,000 conforming loan:

- 740 FICO : No added loan costs

- 720 FICO : 0.250% increase in loan costs, or $500

- 700 FICO : 0.750% increase in loan costs, or $1,500

- 680 FICO : 1.500% increase in loan costs, or $3,000

- 660 FICO : 2.500% increase in loan costs, or $5,000

It’s expensive to have a low credit score — more expensive than the money saved by opening a card at the mall, anyway. Pretty interesting prospective, right?

With that said, if you know you won’t need your credit for a mortgage within the next 6 months, the risk of applying for in-store credit cards is likely small. But if you’ll need your FICO soon, consider paying for your gifts full price. You’ll be really glad you did.

If you’re currently needing a loan or know someone that is, I’d be happy to help you crunch the numbers! As it turns out, I am now in the mortgage business and not the retail world!