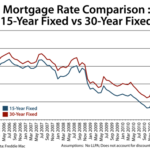

Both Option’s Rates are Sitting at all Time Lows

It’s not just 30-year fixed rate mortgages that are posting all-time lows these days. The 15-year mortgage has been plunging, too.

If you’ve ever considered a 15-year loan term, it’s a terrific time to talk to your lender. According to Freddie Mac’s weekly mortgage rate survey of roughly 125 U.S. lenders, at 3.30 percent, the 15-year fixed rate mortgage is at its lowest point in history.

The 3.30% rate doesn’t come for free, however. Based on average loan term nationwide, borrowers in Iowa choosing to “go 15” should expect to pay 0.6 discount points at closing. 1 discount point is equal to 1 percent of your loan size.

With low rates, 15-year fixed rate mortgage can be enticing; a primary benefit is the huge reduction in the long-term interest costs of your loan. The downside, though, is that monthly mortgage payments can be relatively large.

Save on Interest with 15-Year Fixed Loans

At today’s mortgage rates, a 15-year fixed rate loan carries a principal + interest payment of $705.10 per $100,000 borrowed — a 46% increase over a comparable 30-year fixed rate loan. If you can manage the bigger payments, though, you’ll reap $47,000 in interest payments savings per $100,000 borrowed in paying off your loan in full.

$47,000 per $100,000 borrowed is a huge amount of savings and those saved monies can be used to fund items such as college, home improvement, and retirement, among others.

That said, the 15-year fixed rate mortgage is not for everyone.

Because it comes with higher monthly payments, the 15-year fixed rate mortgage may add financial stress to your household budget. And, once you have committed to a 15-year loan term and its payments, you’re can’t “go back”. Your lender won’t revert your loan to a 30-year schedule without a refinance, and a refinance could be costly.

Related Posts

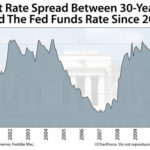

Fed Adjourns Today, Expect Rates to be on the Move

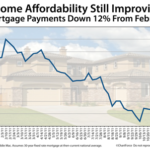

Fed Adjourns Today, Expect Rates to be on the Move House Payments Rise and Fall with Mortgage Rates

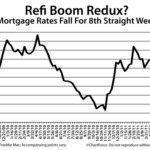

House Payments Rise and Fall with Mortgage Rates Start of A Refi Boom? Mortgage Rates Fall For 8 Straight Weeks

Start of A Refi Boom? Mortgage Rates Fall For 8 Straight Weeks 15-Year Fixed Rate Mortgages Look Cheap Compared To Comparable 30-Year Fixeds

15-Year Fixed Rate Mortgages Look Cheap Compared To Comparable 30-Year Fixeds The Federal Reserve Statement Simplified

The Federal Reserve Statement Simplified Mortgage Rates Continue to Dip Lower and Lower

Mortgage Rates Continue to Dip Lower and Lower