If You Didn’t Notice, Interest Rates Remain Inverted

This is a market condition in which the longer you commit to lending your money, the less that you earn on your investment.

So, “Why is that a big deal?” You Might Ask

Imagine if a friend asked you to borrow money for two years you charged him interest on that money. Let’s look at some of the risks in lending to your friend:

- The risk of not getting paid back

- The risk that the money could have earned more for you somewhere else

- The risk that the value of the dollar will be lower when you get your money back

The more risk you take, the higher the interest rate you should expect on your money. This is a basic principal of finance.

Now, if that same friend wanted the money for 10 years instead of 2 years, you would expect that your risks would be higher across the board.

- He could lose his ability to repay you in those 10 years

- You could have had countless other investment opportunities over those 10 years

- The value of the dollar could swing wildly in those 10 years

Your theoretical risk is much, much higher because your money is tied up for longer periods of time.

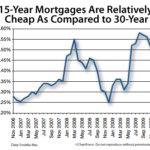

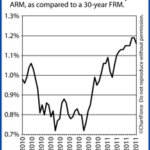

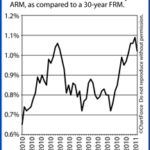

How big of an impact is this having on mortgage rates?

Three years ago, the spread between a 3-year ARM and a 30-year fixed mortgage was about 1.875%. Today, that spread is negative 0.375% – 0.5%.

So, this is why mortgage rates are higher on adjustable rate mortgages (a.k.a. ARM). It’s not voodo financing, it’s and explainable and understandable market condition.

If you’re currently looking at purchasing or refinancing a home, don’t hesitate to run questions by me. I know stuff!