What Makes Up Your Credit Score?

Since 2007, mortgage lenders have clamped down in many areas of underwriting, but none more so than in the area of credit scoring.

Minimum FICO levels are up 120 points or more and conforming mortgage lenders now levy large fees on borrowers whose scores are below 740.

Keeping your credit scores high is a worthwhile goal, but it’s not always easy to do — especially when you don’t know the ins-and-out of how the credit scoring system works.

The Wall Street Journal wrote a terrific piece on credit scoring this week. It’s full of helpful, relevant tips for home buyers, homeowners, and everyone else.

Having Good Credit Will Save You Money

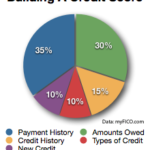

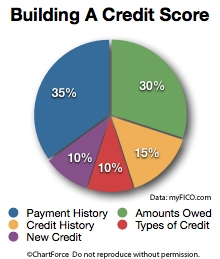

Aside from covering the five basic components of a credit score — shown at right — the piece provides insightful advice on credit-related topics including:

- The difference between a “hard inquiry” and a “soft inquiry”

- Why paying for your credit report is a foolish use of funds

- Why it doesn’t matter if you have an 800 FICO

The article also talks about the optimal balance a person should carry on their credit cards to get the biggest FICO boost.

Credit scores determine your mortgage rate. Therefore, do what you can to keep your scores high. Follow the tips in the Wall Street Journal article and lean on public resources like myFICO.com.

Having good credit can be a real money-saver. Month after month after month.