January 27th 2010 — FOMC Meeting

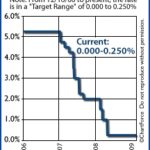

On Tuesday, the Federal Open Market Committee decided to leave the Fed Funds Rate within its target range of 0.000-0.250 percent.

In the Fed’s press release, it was noted that the U.S. economy “has continued to strengthen”, that the jobs markets is getting better, and that financial markets are supportive of growth.

I generally agree with all of these statements.

However, there was no mention of the housing market’s strength. The last 3 statements from the Fed included that specific verbiage. Was that intentional? Your guess is as good as mine.

Most importantly, it’s the fifth straight statement in which the Fed spoke about the economy with optimism. This should signal to markets that 2008 and 2009 recession is over and that economic growth is returning to U.S. economy.

The Fed is Still Optimistic

The economy isn’t without threats, however, and the Fed identified several important points in its press release, including:

- Consumer credit remains tight

- Businesses are still reluctant to hire new workers

- Housing wealth is down (shocker….)

The message’s overall tone did seem positive and inflation appears is still within tolerance. Which again, is a *very* big deal when it comes to mortgage rates.

Most Importantly

Also in its statement, the Fed confirmed its plan to hold the Fed Funds Rate near zero percent “for an extended period” and to wind down its $1.25 trillion commitment to the mortgage market by March 31, 2010. This is extremely noteworthy because Fed insiders estimate that the bond-buying program suppressed mortgage rates by one percent through 2009.

Mortgage market reaction to the Fed press release is, in general, negative. Mortgage rates in Iowa are rose this afternoon.

The next Fed meeting is scheduled for 3/16/2010.

If you’re currently monitoring mortgage rates, I’d love to help give you my insight on your personal situation. I’d love to help out!