What Changes Are Coming?

For the first time this year, Fannie Mae announced some significant updates to its mortgage underwriting guidelines.

For the first time this year, Fannie Mae announced some significant updates to its mortgage underwriting guidelines.

Some of the changes include newer, harsher adjustable rate mortgage qualification standards, and the elimination of a once-popular loan product, and somewhat tighter rules for interest only mortgages.

Fannie Mae made its official announcement (click to see) April 30, 2010. The changes will roll out to home buyers and homeowners in Urbandale and everywhere else over the following 12 weeks.

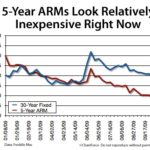

The first guideline change is tied to ARMs specifically 5 years or less.

Mortgage applicants must now qualify based on a mortgage rate based on 2% higher than their note rate. For example, if your mortgage rate (the one you lock) is 5 percent, for qualification purposes, your rate would be 7 percent. As you could imagine, they want to make sure you qualify once rates increase.

The higher qualifying payment will disqualify borrowers whose debt-to-income levels are borderline. In my opinion, it’s good news.

Qualifying Just Got Harder

The second change is Fannie Mae’s elimination of the basic 7-year balloon mortgage. Balloon mortgages were popular early last decade. Lately, few borrowers have chosen to go with them. Mostly because rates have been relatively high as compared to a comparable 7-year ARM. Weird, right?

And, Fannie Mae is changing its interest only mortgages guidelines. Keep reading…

Effective June 19, 2010, Fannie Mae interest only mortgages must meet the following:

- The home must be a 1-unit property

- The home must be a primary residence, or vacation home (no investment properties)

- The borrower’s FICO must be 720 or higher

- The mortgage must be a purchase, or rate-and-term refinance. No “cash out” allowed.

Furthermore, borrowers using interest only mortgages must show two full years of mortgage payments “in the bank” at the time of closing. THAT is a BIG change.

Earlier this year, Fannie Mae-sister Freddie Mac announced that as of September 2010, it will stop offering interest only loans altogether.

Between Fannie Mae, Freddie Mac, the FHA, and other government-supported entities, the U.S. government now backs 96.5 percent of the U.S. mortgage market. So long as mortgage default rates are high, expect approvals for all borrower types to continue to toughen.

If you’re currently getting a mortgage and are wondering how upcoming changes might impact you, please feel free to email me. I’d be happy to help you!