Are You the Right Fit for an ARM Loan?

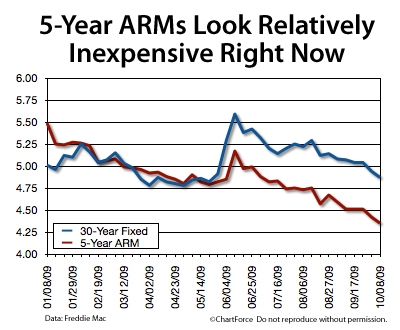

According to the Freddie Mac weekly mortgage rate survey, the relative cost of a 5-year ARM is dropping versus its 30-year fixed-rate cousin.

During the first 5 months of 2009, the products ran neck-and-neck. Today, they’re a half-percent apart.

On a $200,000 home loan, that’s a difference of $60 per month.

Adjustable-rate mortgages aren’t for everyone, but for the right household, they can be a terrific fit. A few scenarios that warrant consideration of a 5-year ARM include persons:

- Buying a home with an intent to sell within 5 years

- With a 30-year fixed mortgage and plans to sell within 5 years

- Interested in low payments and comfortable with longer-term interest rate and payment uncertainty

Make an Informed Decision

Additionally, with homeowners with existing ARMs may want to consider taking on a new ARM, if only to extend their initial, fixed rate period.

Before choosing an ARM, make sure to speak with your loan officer about how adjustable-rate mortgages work, and what causes them to adjust. Although conventional ARMs are limited in how far they can adjust, it’s important to know the risks.

Related Posts

Loan Approvals Are Changing. What Does It Mean For You?

Loan Approvals Are Changing. What Does It Mean For You? Rates Fall to all Time Lows on Adjustable Rate Mortgages

Rates Fall to all Time Lows on Adjustable Rate Mortgages Monthly Mortgage Payments Down 13% Since February 2011

Monthly Mortgage Payments Down 13% Since February 2011 What’s the Difference Between a 15 Year and a 30 Year Fixed Rate?

What’s the Difference Between a 15 Year and a 30 Year Fixed Rate? House Payments Rise and Fall with Mortgage Rates

House Payments Rise and Fall with Mortgage Rates Start of A Refi Boom? Mortgage Rates Fall For 8 Straight Weeks

Start of A Refi Boom? Mortgage Rates Fall For 8 Straight Weeks