Your Interest Rate & APR Are NOT the Same

APR is an acronym for Annual Percentage Rate. It’s a government-mandated calculation meant to simplify the comparison of mortgage options.

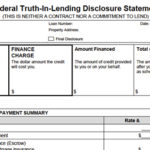

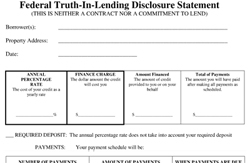

A loan’s APR can always be found in the top-left corner of the Federal Truth-In-Lending Disclosure.

Because APR is expressed as a percentage, many people confuse it for the loan’s interest rate. It’s not. APR represents the total cost of borrowing over the life of a loan. “Interest rate” is the basis for monthly mortgage repayments.

The main advantage of APR is that it allows an “apples-to-apples” comparison between loan products.

As an example, a 5.000 percent mortgage with origination points and fees will almost certainly have a higher APR than a 5.500 percent mortgage with zero fees. In this sense, APR can help a borrower determine which loan is least costly long-term.

An APR Isn’t Always Your Best Comparison Option

First, different banks includes different fees into their APR calculations. By definition, this spoils APR as a choose-between-lenders, apples-to-apples comparison method.

And, second, when calculating APR, “life of the loan” is assumed to be full-term. When a 30-year mortgage pays off in 7 years or fewer — as most of them do — APR comparisons are rendered moot.

In other words, APR is just one metric to compare mortgages — it’s not the only metric. The best way to compare your mortgage options is to review all the loan terms together and determine which is most suitable.