The Announcement

On July 14th, 2008 FHA will be changing a few things with private mortgage insurance (PMI). Just like Fannie Mae made mortgages higher cost, FHA is now following suit. Just in a slightly different way. Once again, they are also placing a heavy focus on credit scores and charging more for credit scores that fall below 680. Yes, this is a pretty long post – but cruise it and get out of it what you need. If you’re an FHA candidate, this will show you how much more money you’ll pay in PMI. If you’re what I call an ‘Advisor’ (such as a realtor, CPA, financial planner, parent or a really well networked person) you’ll be able to tell the people you care about how the changes effect them. So, have you bought in? Read on my friend, read on!

How’s it Work Now?

Currently, there are two different types of PMI on an FHA loan.

- Upfront mortgage insurance premium

Currently is 1.5% of the loan amount and is paid at closing.

For example: $100,000 loan.

$100,000 x .015 = 1,500

Your Upfront MIP (mortgage insurance premium) is $1,500. - Monthly mortgage insurance

Currently the factor is .50%

For example: $100,000 loan.

$100,000 x .05 / 12 = $60

Monthly PMI would be $60

So What Changes July 17th, 2008?

- Borrowers with either no score or at least 500 may get a loan up to 90% of the purchase price/appraised value (see matrix below).

- Borrowers with a score less than 500 get a loan up to 90% of the purchase price/appraised value.

- Borrowers without scores will now require manual underwriting.

- Upfront Mortgage Insurance Premiums will now range from 1.25% to 2.25%, depending on FICO score.

- The Monthly Mortgage Insurance will range from .50% to .55% depending on FICO score.

- The premium is based on the borrower with the lowest FICO score.

- If one of the borrowers has no FICO score, then the Non-Traditional credit grade is used.

- Credit rescoring (a.k.a. rapid re-score) is allowed to improve a borrower’s credit grade.

- All FHA Secure refinances over 95% of appraised value with delinquencies will have a 2.25% up front MIP and .55% monthly PMI.

- Along with purchases, these changes apply to cash-out, rate & term, and non-delinquent FHA Secure refinances.

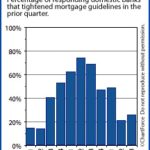

Visual Aid

Explanation of Visual Aid

- The column on the far left indicates the ‘Loan-to-Value’. Simply said, it’s the percentage of the appraised value (in a refinance) or purchase price (on a purchase).

- Across the top there are FICO score ranges.

Using The Chart to See How the Changes Will Effect You

To determine what type of mortgage insurance you’ll have to pay on your FHA loan, you must first know the answers to the following questions.

- How much money will you be putting down or how much equity do you have in your home? Then, determine the loan to value percentage based on that.

- What is your lowest FICO score? (lowest of all three)

Now you’re ready to read the new chart. You’ll first find your ‘Loan-to-Value’. Then from that column move across to the right and find your credit score column.

Okay. Let’s say you’re financing 97% on a purchase and you have a 602 FICO score. You’ll see the chart says “175/55”. Here’s how it calculates:

- “175” indicates your up front MIP.

1.75% of the loan amount is paid up front.

Example: $100,000 loan amount

$100,000 x .0175 = 1,750

Your Upfront MIP (mortgage insurance premium) is $1,750. - “55” indicates your monthly PMI.

.55 is your factor.

Example: $100,000 loan amount

$100,000 x .0055 / 12 = $66

Monthly PMI would be $66

How much more does it cost? Well, in this example – you’re spending $250 more in up front MIP and $6 per month. Over 5 years, this loan will cost $610 more. Keep in mind it’s a super conservative loan amount of $100,000 and a decent credit score.

If you had a 550 FICO score, getting the same loan – the new mortgage insurance standards will cost you $1,110 more than it currently (I am writing this June 17th, 2008) would cost. Pretty significant.

In Closing

Here’s the thing, getting 97% financing when you have a credit score below 680 is pretty phenomenal to begin with. We can’t complain that FHA saw some huge risks loaning to higher risk borrowers. Yes, it will cost slightly more to own a home. However, let’s be realistic – this is still a stellar loan. You cannot get it done anywhere else (as we speak).

If you’re on the fence and can act quickly, you may be able to beat the changes. If you’re not even close to being able to close on a home, you might just have to live with these changes either way!

As always, if you have further questions – don’t hesitate to contact us!

Related Posts

New Changes Coming for FHA Streamline Refinances

New Changes Coming for FHA Streamline Refinances FHA Mortgage Insurance Premiums are Rising Again

FHA Mortgage Insurance Premiums are Rising Again 2010 FHA Loan Limits Show No Change from 2009

2010 FHA Loan Limits Show No Change from 2009 You May Want To Get Your FHA Loan Before It’s Too Late!

You May Want To Get Your FHA Loan Before It’s Too Late! FHA Loan Limits are now Higher Than Conventional Loans for 1st Time Ever

FHA Loan Limits are now Higher Than Conventional Loans for 1st Time Ever Banks Raising the Bar on Mortgage Qualifications

Banks Raising the Bar on Mortgage Qualifications

{ 7 comments… read them below or add one }

Thanks for the detailed explanation of FHA’s new PMI guidelines. I have bookmarked it for future client reference.

Roberta – No problem! It’s a story that’s not being told yet. I’d get used to credit risk based pricing (FICO score driven rates and costs) in the future. The mortgage industry is quickly learning that the FICO model has a great way of predicting future delinquencies!

Thanks for reading and please – keep up the encouraging comments! 😉

My understanding is that Congress overrode the FHA proposed rule of risk-based insurance premiums. As a result, everyone gets slapped with the 1.75% fee regardless of credit worthiness.

@T – You’re absolutely right. The difficult thing about a blog is that the information is very time sensitive. I’m glad you brought this up for new readers hitting the site!

Just a re-mention of my comment under ‘Legal’ for the site:

“It goes without saying (but again, this is legal disclosure), the mortgage industry is a changing one. Facts & market information are a moving target and should be reviewed with the market conditions as you read (much of this information is archived from the past). We’d be glad to help you determine if things have changed.”

On my settlement statement I noticed an upfront MIP and I will also be paying a monthly MIP. Is this within the new guidelines?

@Carole – With FHA loans, you’ll have two different types of private mortgage insurance. This isn’t a new addition, FHA has always required both.

1) Up front mortgage insurance policy (a.k.a. UF-MIP). This is added to the loan amount in most situations.

2) Monthly PMI. This is paid on a monthly basis to your mortgage lender and is included in your payment.

I hope this helps! Thanks for joining the conversation.

Any idea how PMI is calculated with FHA now (2011)?

{ 2 trackbacks }