What’s the Difference Between a Fixed Rate Mortgage and an Adjustable Rate Mortgage?

For some homeowners, picking an adjustable rate mortgage (ARM) over a fixed rate one could simply be matter of budgeting. ARMs tend to carry lower mortgage rates and, therefore, lower monthly mortgage payment as compared to a comparable fixed rate loan.

For some homeowners, picking an adjustable rate mortgage (ARM) over a fixed rate one could simply be matter of budgeting. ARMs tend to carry lower mortgage rates and, therefore, lower monthly mortgage payment as compared to a comparable fixed rate loan.

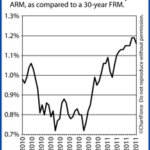

Compared to fixed rate mortgages, current ARM pricing is excellent. Freddie Mac’s weekly Primary Mortgage Market Survey puts the 5-year ARM mortgage rate lower than the 30-year fixed rate mortgage rate by 1.02 percent. Yea, no kidding.

On a $250,000 home loan, a 1.02 differential yields a payment savings of $149 per month. That adds up!

Naturally, ARMs are not for everyone, of course. Over time their rates can change and that often frightens people. An ARM has the potential to finish its respective 30-year lifespan with a mortgage rate as much as 6 percentage points higher from where it started. Some homeowners won’t like this.

Other homeowners, however, won’t mind it. For this group, the ARM can be a terrific fit. Especially with the huge, relative discount in today’s pricing.

Still not sure? Keep reading.

Here Are a Few Scenarios FOR Doing a 5-year ARM:

- Buying a new home with the intent to sell within 5 years

- Currently financed with a 30-year fixed mortgage with plans to sell within 5 years

- Interested in low payments; comfortable with longer-term rate and payment uncertainty

In addition, homeowners with existing ARMs due for adjustment may want to refinance into a new ARM, if only to push the first adjustment date farther into the future. We’ve done a ton of this at my office recently and I’d be happy to help you do it for your loan.

Before choosing to go with an ARM, it’s important to talk to a loan officer about how adjustable rate mortgages work. You need to understand their near- and long-term risks. Payment savings may be tempting, but with an ARM, payments are permanent.

If you’re looking for some help, but not sure who to call, I’d be happy to help. My phone number is on this page or, you can email me (also on the page!). I love to help my readers out with their mortgages!

Related Posts

Rates Fall to all Time Lows on Adjustable Rate Mortgages

Rates Fall to all Time Lows on Adjustable Rate Mortgages How to Avoid Paying a Higher Rate on Your Mortgage

How to Avoid Paying a Higher Rate on Your Mortgage Which is Better? A Fixed Rate or an Adjustable Rate Mortgage?

Which is Better? A Fixed Rate or an Adjustable Rate Mortgage? Mortgage Markets Improved Last Week Due to a Slowing U.S. Economy

Mortgage Markets Improved Last Week Due to a Slowing U.S. Economy A Perfect Example of What a Refinance Could Do for You

A Perfect Example of What a Refinance Could Do for You Why An Inverted Yield Curve Means Higher Rates on Adjustable Rate Mortgages

Why An Inverted Yield Curve Means Higher Rates on Adjustable Rate Mortgages