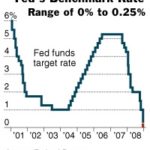

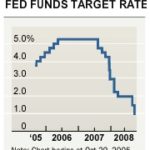

Remember What Caused It

In late-November, the Federal Reserve pledged $600 billion to buy mortgage-backed securities. The announcement drove down mortgage rates and started the ‘first’ Refi Boom.

Then, the Federal Reserve made a second series of statements after its scheduled meeting last Tuesday, causing mortgage rates to plunge again. This started the Refi Boom’s second wave.

Because of the surge in refinance activity, mortgage lenders are “backed up”; initial file reviews are taking up to 12 business days in some cases. Remember, many companies cut back on staff earlier this year when things were slow.

Typically, this underwriting process takes 2 days.

What’s It Mean To You?

Underwriting delays are problem for refinancing Americans because when a mortgage rate is locked, it’s most often locked for 30 calendar days — the standard Rate Lock Agreement contract length. If the mortgage doesn’t close within those 30 days, the applicant must either pay an “extension fee” to preserve the lock, or risk losing the rate altogether. Bad news, right?

30 days may seem like a long time, but let’s consider a few external variables:

- December 24, 25, and 26 plus January 1 and 2 are lost to holiday

- December 27, 28 plus January 3, 4, 10, 11, 17, and 18 are lost to weekends

- January 19 is lost to federal holiday

- 3 days are lost to the Right To Cancel clause

This leaves 13 days to get from Application to Closing, and of those 13 days, 12 of them are being spent on the initial review. A 30-day rate lock, in other words, may be an inadequate agreement with some mortgage lenders. A 45-day agreement may be required instead.

The Bad News About Abnormal Underwriting Turn Times

Typically, 45-day rate locks carry higher rates or higher fees, versus their 30-day counterparts. This amounts to a “tax” on borrowers, a result of the nation’s rush to refinance with the rest of the pack.

As always, the best way to preserve a rate lock is to be as responsive as possible to the process. Return paperwork when asked, schedule appraisals immediately, and arrange to signing closing paperwork on the first available day. NO slacking. There simply isn’t time for it.

With mortgage rates low, application volume — and underwriting turntimes — should remain high into early-2009. There will be booms to follow in 2009.