When Selling a Home You Have Options

When a homeowner sells their home and decide to buy a new one, there are 3 basic options for the residence:

- Sell it.

- Keep it.

- Rent it.

Things Are Changing

Unfortunately, no matter which path they choose, move-up homebuyers looking for a new conforming mortgage will find qualifying for a home loan to be more difficult this season than in the past.

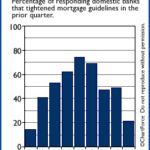

Mortgage guidelines are dramatically tighter for people “carrying two mortgages”.

Among the changes this spring’s buyers face:

Selling the primary residence

If you plan to close on your new home prior to the closing of your existing home — even if it’s only by a day — both payments must be listed as monthly debts on your mortgage application. This will disqualify the majority of homebuyers. It’s treated as if you kept both homes.Converting your residence to a second home

If your current home has less than 30 percent equity in it (ex. owing 70,000 or less on a 100,000 home), your mortgage application for the new home will not be approved unless you can show 6 months worth of mortgage payments + taxes + insurance in reserves for the current home and new home combined.Converting your residence to an investment property

If your current home has less than 30 percent equity in it (again.. ex. owing 70,000 or less on a 100,000 home), any rental income derived from a tenant is disallowed on your mortgage application for the new home. You must still count the mortgage payment + taxes + insurance as a monthly debt.

Knowing The New Rules Is Important and It Could Impact You Big Time!

In other words, being a move-up buyer isn’t as simple as it used to be. New lending rules make buying a new home an exercise in timing and financial planning. And the rules are expected to get tougher, too.

Therefore, if you expect to be a move-up buyer in the next 12 months, consider moving up your timeframe or — at least — planning ahead for it.

Understanding the new mortgage landscape and how they can influence your upcoming purchase may be the difference between getting approved for a home loan, and getting turned down.