Approvals Are Getting Harder to Come By

Despite the economy’s improvement and prodding from Congress, banks don’t seem ready to open their purse strings just yet.

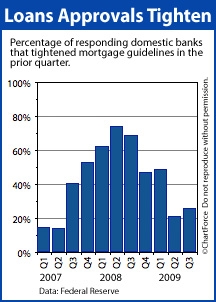

Nationally, mortgage approval standards are tightening.

The data comes from a quarterly survey the Federal Reserve sends to its member banks. The Fed asks senior bank loan officers around the country whether “prime” residential mortgage guidelines had tightened in the last 3 months.

For the period July-September 2009:

- Roughly 1 in 4 banks said guidelines tightened

- Roughly 3 in 4 banks said guidelines were “basically unchanged”

Just one bank said its guidelines had loosened.

If You’re on the Fence, Now May be the Time to Act

Combine the Fed’s survey with recent underwriting updates from the FHA and from Fannie Mae and it becomes clear that mortgage lenders are much more cautious about their loans than they were, say, 2 years ago.

Today’s borrowers face a host of hurdles including:

- Higher minimum FICO scores

- Larger downpayment requirements for purchases

- Larger equity positions for refinances

- Lower debt-to-income ratios

In other words, mortgage rates may stay low into 2010, but that won’t matter to homeowners that don’t meet minimum eligibility standards. With each passing quarter, that list gets smaller.

Therefore, if you’re on the fence about whether now is a good time to buy a home, remember that, along with an increase in mortgage approval standards, home values are rising, too.

Acting sooner is probably better than acting later.

Related Posts

New Changes Coming for FHA Streamline Refinances

New Changes Coming for FHA Streamline Refinances FHA Mortgage Insurance Premiums are Rising Again

FHA Mortgage Insurance Premiums are Rising Again FHA Loan Limits are now Higher Than Conventional Loans for 1st Time Ever

FHA Loan Limits are now Higher Than Conventional Loans for 1st Time Ever New Loan Limits to Take Effect October 1, 2011

New Loan Limits to Take Effect October 1, 2011 FHA Mortgage Insurance Premiums Rising .25% on April 18th

FHA Mortgage Insurance Premiums Rising .25% on April 18th FHA Streamline Refi Changes : For the Better!

FHA Streamline Refi Changes : For the Better!