Pay More Per Month but Save Money in the Long Run

For today’s home buyers and homeowners that can manage the higher monthly payments, 15-year fixed rate mortgage rates look attractive as compared to comparable 30-year products.

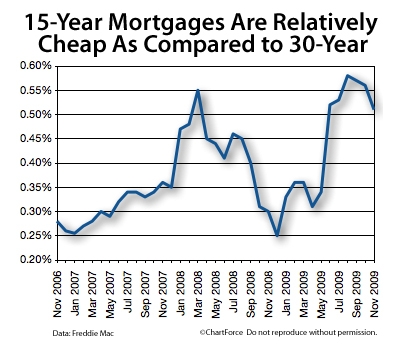

The 15-year/30-year interest rate spread is near its 5-year high.

Despite lower rates, however, homeowners opting for a 15-year fixed mortgage should be prepared for its higher monthly payments. This is because the principal balance of a 15-year fixed is repaid in half the years as with a standard, 30-year amortizing product.

As compared to 30-year terms, 15-year products repay 3 times as much principal each month.

There Are Downsides Too

Versus a 30-year, 15-year fixed mortgages have a few downsides worth noting. The first is that, because 15-year mortgages are heavy on principal and light on interest, homeowners who itemize tax returns may have to claim a smaller mortgage interest tax deduction at tax time.

Another negative is that the sheer size of the payment. If you run into fiscal trouble down the road, the only way to reduce the monthly obligation is to refinance into a 30-year product and that costs money to do.

In other words, be sure you can manage the payments over the long-term before you opt for a 15-year term. If you can manage it, though, the rewards are tangible.

At today’s rates, a 15-year fixed and 30-year fixed costs $230 extra per $100,000 borrowed.

Related Posts

Why An Inverted Yield Curve Means Higher Rates on Adjustable Rate Mortgages

Why An Inverted Yield Curve Means Higher Rates on Adjustable Rate Mortgages How to get rid of PMI and stop lighting your money on fire

How to get rid of PMI and stop lighting your money on fire Rates Fall to all Time Lows on Adjustable Rate Mortgages

Rates Fall to all Time Lows on Adjustable Rate Mortgages Loan Approvals Are Changing. What Does It Mean For You?

Loan Approvals Are Changing. What Does It Mean For You? Real Estate Definition: Escrow Account

Real Estate Definition: Escrow Account Home sales are up 12%. Now for the bad news…

Home sales are up 12%. Now for the bad news…